Foreign Tax Credit for Non-Permanent Residents in Japan

【Koshida Accounting Firm Column Date:】

Hello, my name is Taisei Koshida, and I am a Certified Public Accountant and Licensed Tax Accountant in Japan.

I specialize in helping foreign business owners and individuals with Japanese tax matters, especially those who need assistance in English.

Many non-permanent residents living in Japan are surprised to learn that claiming a foreign tax credit is not as simple as paying tax overseas.

Whether you can claim a foreign tax credit depends on several factors, including whether remittance-based taxation applies and when the foreign tax is actually paid.

This article explains the basic steps for determining whether a foreign tax credit is available in Japan.

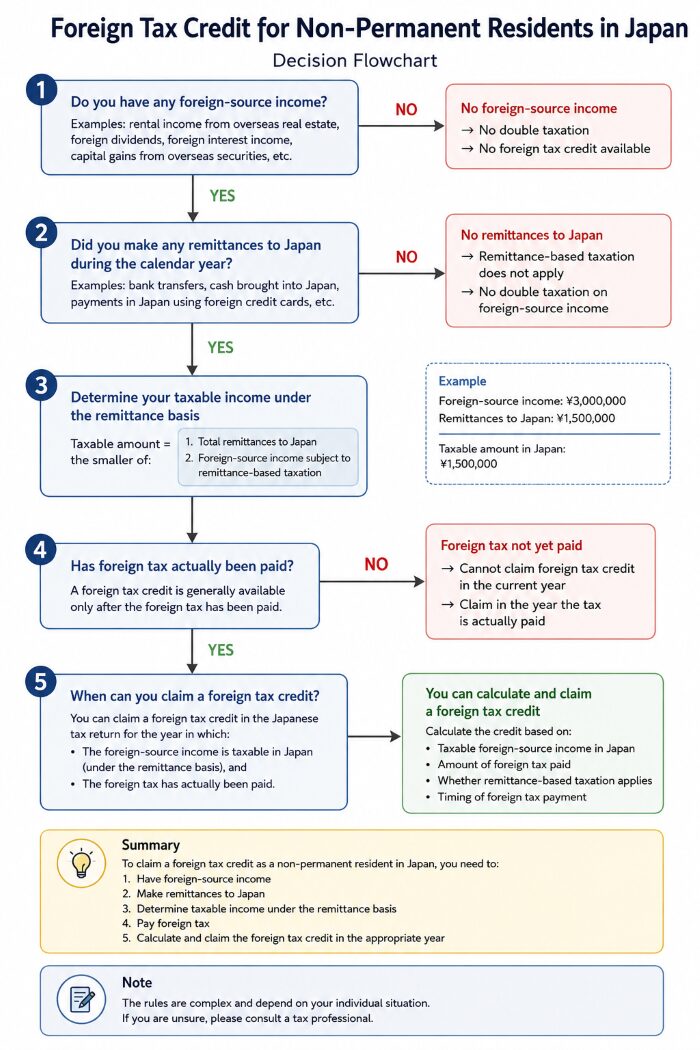

Decision Flow for Claiming a Foreign Tax Credit as a Non-Permanent Resident in Japan

1. Do You Have Foreign-Source Income?

The first step is to determine whether you have any foreign-source income.

Typical examples of foreign-source income include:

- ・Rental income from overseas real estate

- ・Foreign dividends

- ・Foreign interest income

- ・Capital gains from overseas securities

One point is frequently misunderstood.

Even if your salary is paid by a foreign company, it may still be treated as Japanese-source income if you physically perform the work while living in Japan, such as working remotely from Japan.

If you have no foreign-source income, there is generally no double taxation and therefore no foreign tax credit available.

2. Did You Remit Funds to Japan?

If you have foreign-source income, the next step is to determine whether you made any remittances to Japan during the calendar year.

Examples of remittances include:

- ・Bank transfers to Japan

- ・Cash brought into Japan

- ・Payments made in Japan using foreign credit cards

However, certain amounts should be excluded from the calculation, such as payments made from Japanese-source income that happened to be received abroad.

If there were no remittances to Japan during the year, remittance-based taxation generally does not apply, and no double taxation arises on your foreign-source income.

3. Determine Your Taxable Income Under the Remittance Basis

If you made remittances to Japan during the year, the next step is to determine how much of your foreign-source income becomes taxable in Japan.

Under Japan’s remittance-based taxation rules for non-permanent residents, the taxable amount is generally the smaller of:

- ・Your total remittances to Japan during the calendar year, or

- ・Your foreign-source income that is subject to remittance-based taxation.

For example:

- ・Foreign-source income: ¥3,000,000

- ・Remittances to Japan: ¥1,500,000

In this case, only ¥1,500,000 of the foreign-source income becomes taxable in Japan under the remittance basis.

If you have several types of foreign-source income, such as dividends, interest, rental income, and capital gains, the remittance amount generally needs to be allocated among each category before calculating Japanese income tax.

4. Has Foreign Tax Actually Been Paid?

This is one of the most misunderstood aspects of the foreign tax credit.

A foreign tax credit is generally available only after the foreign tax has actually been paid.

For example, suppose you receive dividend income in 2026.

If U.S. withholding tax is deducted immediately, you may generally claim a foreign tax credit in your 2026 Japanese tax return.

However, capital gains are often different.

In many cases, U.S. capital gains tax is not paid until the following year when the U.S. income tax return is filed.

If the U.S. tax relating to your 2026 capital gains is paid in 2027, the foreign tax credit is generally claimed on your 2027 Japanese tax return rather than your 2026 return.

Understanding the timing of foreign tax payments is therefore just as important as calculating your taxable income.

5. When Can You Claim a Foreign Tax Credit?

After determining your taxable foreign-source income and confirming that foreign tax has actually been paid, you can calculate your foreign tax credit.

Unfortunately, the calculation is rarely straightforward.

Among other things, you need to determine:

- ・Which foreign income is taxable in Japan,

- ・How much foreign tax relates to that income,

- ・Whether remittance-based taxation applies, and

- ・Whether the foreign tax was paid during the relevant tax year.

Because these rules interact with one another, the calculation can become complicated even for relatively simple investment portfolios.

Summary

Preparing a Japanese tax return as a non-permanent resident involves much more than simply reporting your income.

You may need to calculate remittances, classify Japanese-source and foreign-source income, determine taxable income under the remittance basis, calculate the Japanese cost basis of your investments, and decide whether a foreign tax credit is available.

In practice, many foreign residents do not realize how complicated these rules are until they prepare their first Japanese tax return.

If you are unsure how the Japanese tax rules apply to your situation, obtaining professional advice may help you avoid unnecessary tax and filing mistakes.

Because every taxpayer’s situation is different, professional advice is often worthwhile, especially if you have multiple sources of foreign income or significant investments overseas.