Consumption Tax on Real Estate Purchases for Private Lodging Businesses in Japan

【Koshida Accounting Firm Column Date:】

Hello, my name is Taisei Koshida, and I am a certified public accountant and tax accountant.

I aim to assist non-Japanese business owners who need help with reading or writing in Japanese. If you find the Japanese tax system challenging, I can help you with your accounting and tax filings.

Starting a private lodging (minpaku) business in Japan often requires purchasing a property. While accommodation fees are generally subject to Japanese consumption tax, many business owners wonder whether they can also recover the consumption tax paid when purchasing the building.

The answer depends on several factors, including who sells the property, how the property is used, and whether your business is registered as a taxable business for consumption tax purposes.

In this article, I explain how Japan’s consumption tax rules apply when purchasing real estate for a private lodging business and when the input consumption tax may become deductible.

If you would like a general overview of Japan’s consumption tax system, please read the following article first.

An Easy Explanation of Consumption Tax for Doing Business in Japan

1. Purchasing Property from a Private Individual

When you purchase real estate from a private individual who is not conducting a taxable business, the sale is generally not subject to Japanese consumption tax.

Because no consumption tax is charged on the purchase price, there is no input consumption tax that can be deducted from the consumption tax payable on your private lodging business.

This rule applies regardless of whether the property will later be used for taxable private lodging operations.

2. Purchasing Property from a Business

When you purchase real estate from a business, the building portion of the purchase price is generally subject to Japanese consumption tax, while the land portion is exempt.

At first glance, it may seem that the consumption tax paid on the building can simply be deducted from the consumption tax you owe. However, the rules are more complicated, and whether you can recover the tax depends on how the property is used and your consumption tax status.

(1) Why the Consumption Tax Is Not Immediately Deductible

A real estate company that purchases properties as inventory for resale can generally deduct the input consumption tax in the year of purchase.

However, different rules apply when you purchase a property for use in your own private lodging business.

Because the building is initially acquired for your own use rather than for resale, the input consumption tax is generally not deductible immediately.

(2) A Deduction May Be Available in the Third Fiscal Year

Under certain conditions, you may be able to recover part or all of the input consumption tax in the third fiscal year after the property was purchased.

The deductible amount is calculated using the following formula.

Deductible Amount

=

Input Consumption Tax Paid on the Building

×

Taxable Sales Generated by the Property During the First Three Fiscal Years

÷

Total Sales Generated by the Property During the First Three Fiscal Years

For example, if the property is used exclusively for a taxable private lodging business and is not rented out as residential housing, the taxable sales ratio will be 100%.

In that case, the entire amount of the input consumption tax paid on the building may become deductible in the third fiscal year.

(3) You Must Be Registered as a Taxable Business

To claim the adjustment in the third fiscal year, your business must have been registered as a taxable business in the fiscal year in which the property was purchased.

Many newly established businesses in Japan are initially exempt from consumption tax. If you remain exempt, you generally cannot claim this adjustment later.

Therefore, if you expect to purchase a property for your private lodging business, you should carefully consider electing taxable business status by submitting the appropriate notification to the tax office within the required deadline.

However, electing taxable business status is not always the best option. Once you become a taxable business, you are generally required to collect and pay consumption tax on your taxable sales. The overall tax impact depends on your expected revenue, expenses, and the purchase price of the property.

(4) Why a Tax Simulation Is Essential

Whether electing taxable business status is beneficial depends on your individual circumstances.

You should compare the total cash flow under both scenarios, including the expected consumption tax payable, any deductible input consumption tax, and possible tax refunds.

Only after performing this simulation can you determine which option will result in the lowest overall tax burden.

Because the amount involved in a real estate purchase is often substantial, choosing the wrong option could cost hundreds of thousands or even millions of yen. Professional tax planning before purchasing the property can therefore make a significant financial difference.

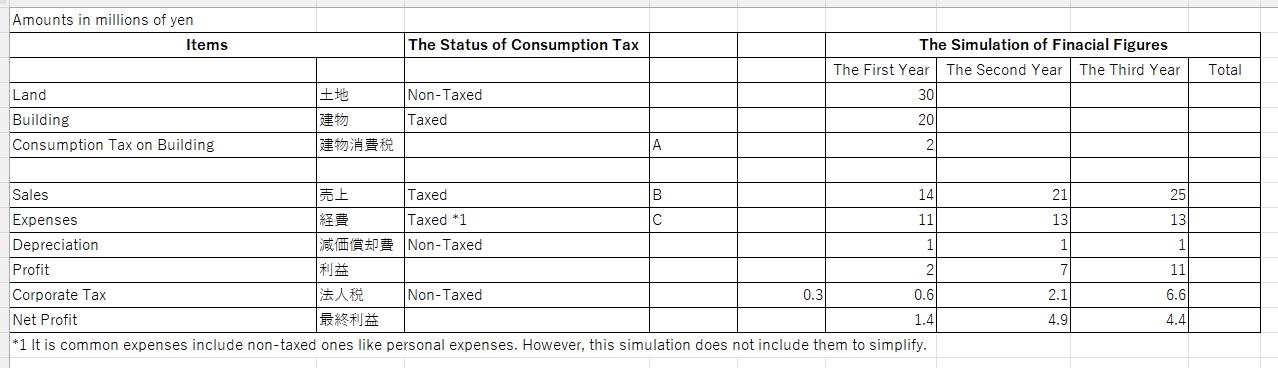

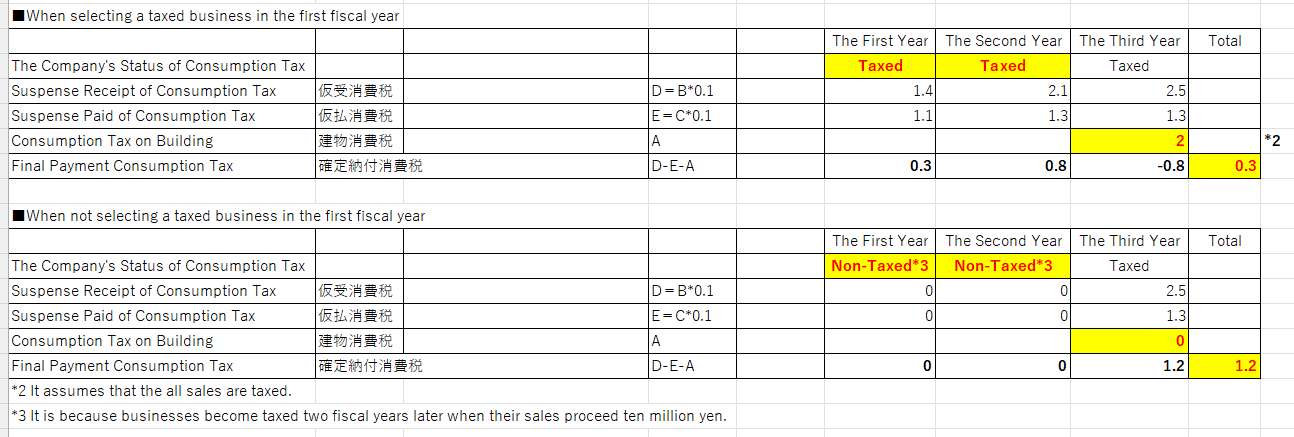

The following simplified example compares the total consumption tax burden over the first three fiscal years under two different scenarios.

The example below compares:

• Electing taxable business status from the first fiscal year

and

• Remaining exempt from consumption tax

In this simplified example, the total consumption tax burden over the first three fiscal years is approximately ¥300,000 when taxable business status is elected, compared with approximately ¥1.2 million when the business remains exempt.

In other words, electing taxable business status produces a significantly better financial outcome in this example.

However, every business is different. The most advantageous option depends on your expected revenue, expenses, and investment plan.

6. Frequently Asked Questions

Can I recover the consumption tax when purchasing a property for a private lodging business?

It depends.

If you purchase the property from a business, the building portion is generally subject to Japanese consumption tax. However, whether you can recover that tax depends on several factors, including how the property is used and whether your business is registered as a taxable business.

Does land include consumption tax?

No.

In Japan, land transactions are generally exempt from consumption tax. Only the building portion of the purchase price is normally subject to consumption tax.

Can I deduct the consumption tax immediately after purchasing the property?

Not usually.

If the property is purchased for use in your own private lodging business, the input consumption tax is generally not deductible immediately. Under certain conditions, an adjustment may become available in the third fiscal year.

Should every private lodging business elect taxable business status?

Not necessarily.

Electing taxable business status can reduce your overall tax burden in some cases, but it also requires you to collect and pay consumption tax on your taxable sales. A tax simulation is recommended before making the decision.

Is professional advice recommended before purchasing a property?

Yes.

Because purchasing real estate often involves a significant amount of consumption tax, careful tax planning before the purchase can potentially save a substantial amount of money.

Our accounting and tax office has extensive experience assisting foreign business owners with Japanese accounting and tax matters.

In addition to tax and accounting services, we work closely with trusted specialists in visa applications, company registration, social insurance, legal services, web marketing, website development, and business consulting. This allows us to provide comprehensive support for starting and operating a business in Japan.

All of our services are available in English.

If you are planning to purchase property for a private lodging business or would like advice on Japan’s consumption tax rules, please feel free to contact us through our inquiry form.